BY CBRE RESEARCH TEAM | ORIGINALLY PUBLISHED ON DECEMBER 13, 2022 | CBRE

Overview: A Challenging Year Ahead

High interest rates and a recession will make 2023 a challenging year for commercial real estate. Though inflation eased in late 2022, it was still running at more than 7%. The Fed will continue raising rates until it sees a marked reduction in inflation nearer to its 2% target. Weakening fundamentals and higher cost of capital will generally lower asset values.

The recession will not be particularly deep. Corporate finances are in good shape and employers will shun excessive layoffs to avoid losing employees in a tight market for skilled labor. While consumer confidence is highly subdued, average household debt is low compared with the onset of previous recessions. These factors suggest a moderate downturn, with unemployment unlikely to breach the 6% level. Inflation will be significantly lower by the second half of 2023, setting the stage for falling interest rates and the beginning of a new cycle that will last to the 2030s.

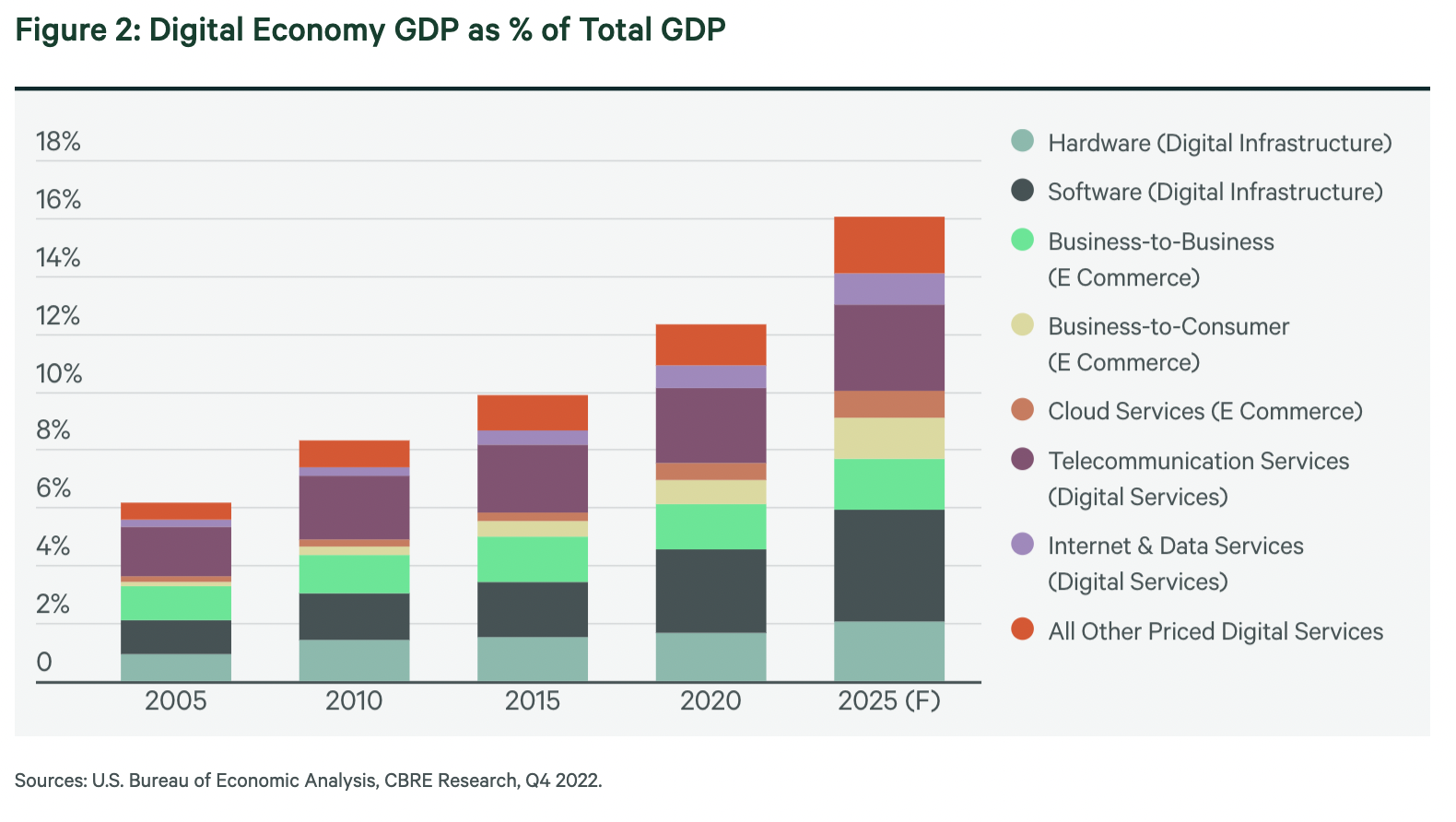

Despite economic headwinds, the pace of change will not ease. ESG considerations and the growth of the digital economy will continue to affect real estate demand. Hybrid working offers many benefits for businesses and employees, but companies and the office sector will have to evolve. Cities too will need to adjust to new commuting patterns and reduced office demand. The resurgent retail sector is just now reaping the benefits of a long period of change, which is attracting keen investor interest. Data centers and industrial real estate will probably be the most resilient sectors and the housing shortage will benefit the multifamily sector. The hotel sector’s recovery from pandemic restrictions will continue but life sciences activity, which was turbocharged by COVID, will ease for a while as venture capital becomes scarcer. All sectors in all places will be required by governments, occupiers and investors to make significant decarbonization efforts.

Our 2023 outlook details the major trends that will dominate the year. Should you have any questions about how these trends may impact your specific real estate strategy, please don’t hesitate to contact us.

Richard Barkham

Global Chief Economist & Global Head of Research

Chapter 2 Economy & Policy

U.S. faces recession in 2023

Sharply higher interest rates will weigh on the U.S. economy in 2023. House prices and retail sales will decline and unemployment will rise. The U.S. dollar’s continued strength against other global currencies will further squeeze corporate earnings and export sales, limiting business investment. As a result, CBRE expects a recession in 2023, resulting in less real estate investment and leasing activity. Adding to the contractionary effects of tighter monetary policy is a weaker global economy. Elevated energy prices, the war in Ukraine and weaker housing demand will inhibit growth in 2023.

Although we expect a recession, we are not overly pessimistic. The U.S. consumer has low leverage and a relatively strong balance sheet. The digital economy and the reshoring of manufacturing—particularly semiconductor production—are two significant growth drivers.

Declining inflation in 2023 will provide a tailwind for the economy toward the end of the year. While the drop will be gradual and bumpy, CBRE forecasts that a slowdown in consumer demand, the easing of global supply chain bottlenecks and a weaker housing market will push inflation down to around 3% by year’s end. We expect that the Federal Reserve will scale back its rate hikes after interest rates peak at 5.2%. The economy should stabilize by the start of 2024 but the downturn’s impact on real estate will linger until employment growth resumes. For the first time in a decade, there is a chance of a buyer’s market in real estate.

Geopolitical improvements could ease recession’s impact

Assuming the Ukraine-Russia war ends next year, as many expect, commodity and food prices should come down. Energy prices will fall, though will not return to pre-war levels as countries continue to seek alternatives to Russian energy sources. China will continue to grapple with COVID, weakness in its housing market and structural shifts in its economy. However, it does not have to deal with high inflation and its current round of stimulus will boost growth in the Asia-Pacific region.

Risks and opportunities from recession

The precise fallout from rapidly rising interest rates is hard to predict, which in turn creates risk. Risky financial positions established amid the past decade’s ultra-low-interest-rate environment may be unsustainable, creating conditions for a financial shock that could lead to a credit crunch. This most likely will occur in highly indebted emerging markets, particularly in Latin America. On the upside, inflation in the U.S. could fall more quickly than expected as supply constraints ease and retailers move into deep discount mode.

Will higher interest rates significantly lower real estate prices?

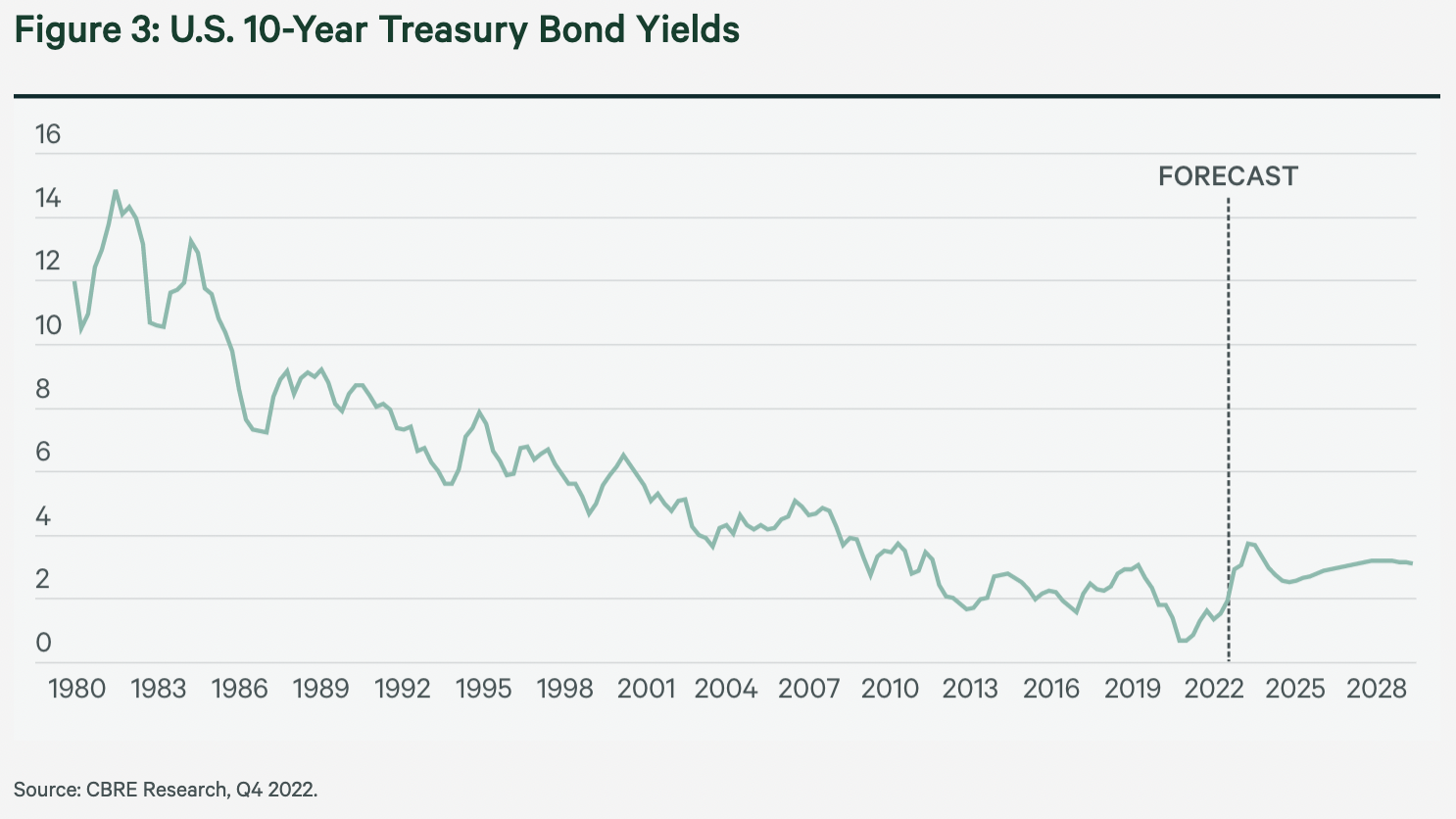

There are concerns that real estate could be permanently repriced if interest rates remain high for the long run. This is unlikely. Long-term interest rates—typically measured by the 10-year U.S. Treasury yield—are driven by inflation expectations, the real interest rate and the “term premium”.

Inflation expectations should fall over the course of 2023 near the Federal Reserve’s 2% target. The real interest rate, determined by the supply and demand for capital in the global economy, likely won’t rise significantly due to demographic factors. The term premium is small and should remain constant.

In CBRE’s view, the 10-year U.S. Treasury yield will increase to around 3% from the 2.2% average over the past decade but will not be large enough to materially alter the investment landscape or fundamentally reset real estate asset values in the long term.

Chapter 3 Capital Markets

Investment activity, asset values expected to drop

The slowdown in commercial real estate investment activity that began in the second half of 2022 will continue in the first half of 2023. Financing may be difficult to obtain as the cost of capital increases and lender appetite diminishes amid volatility in financial markets. However, capital is available for the right deals, such as high-quality multifamily, industrial and grocery-anchored retail, or with established, creditworthy borrowers. CBRE expects lenders will become more active as the macro-economic environment improves and interest rates stabilize.

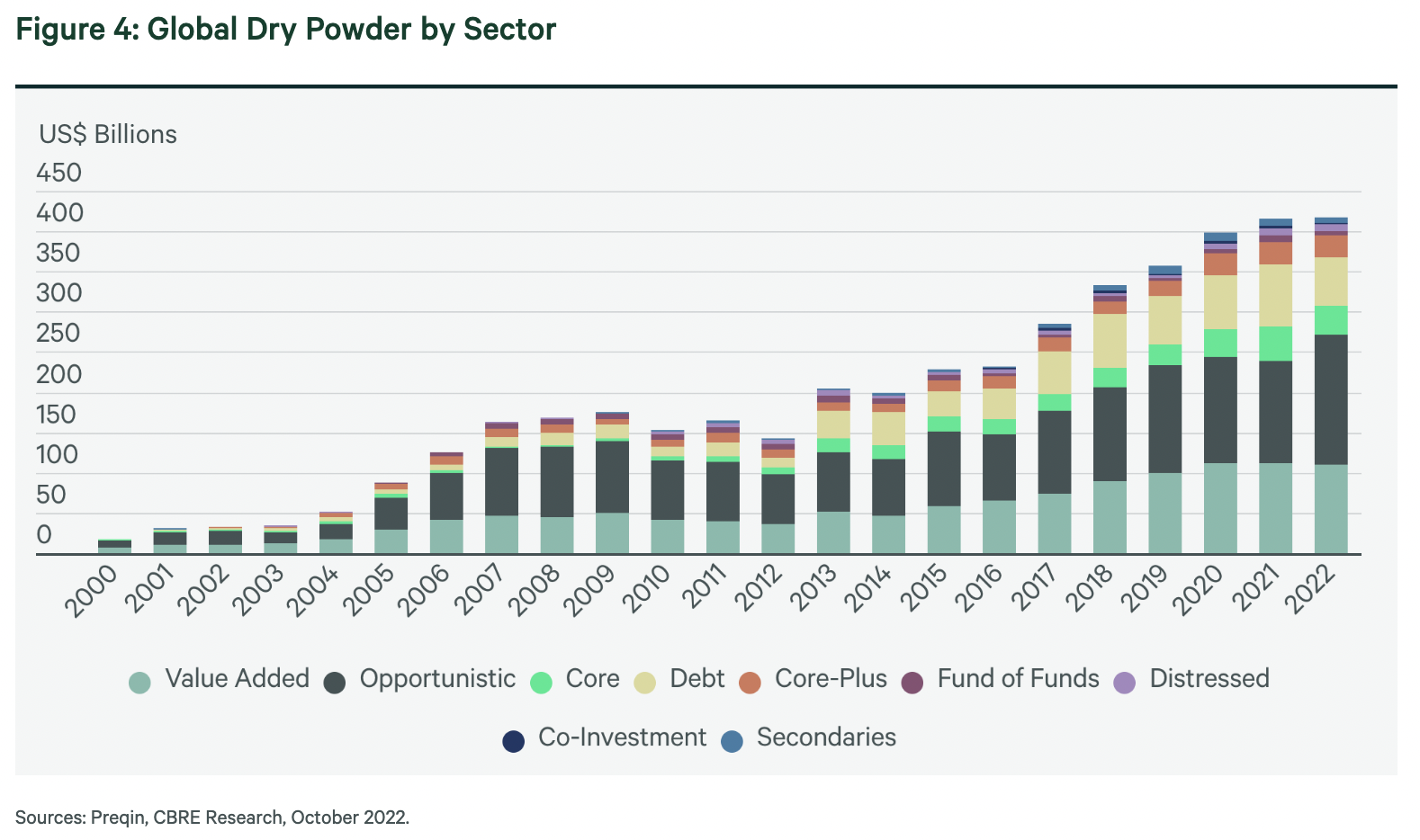

The market will also benefit from the near-record amounts of equity capital that continue to target real estate investment despite the prospect of a moderate recession next year.

Rising interest rates to impact values

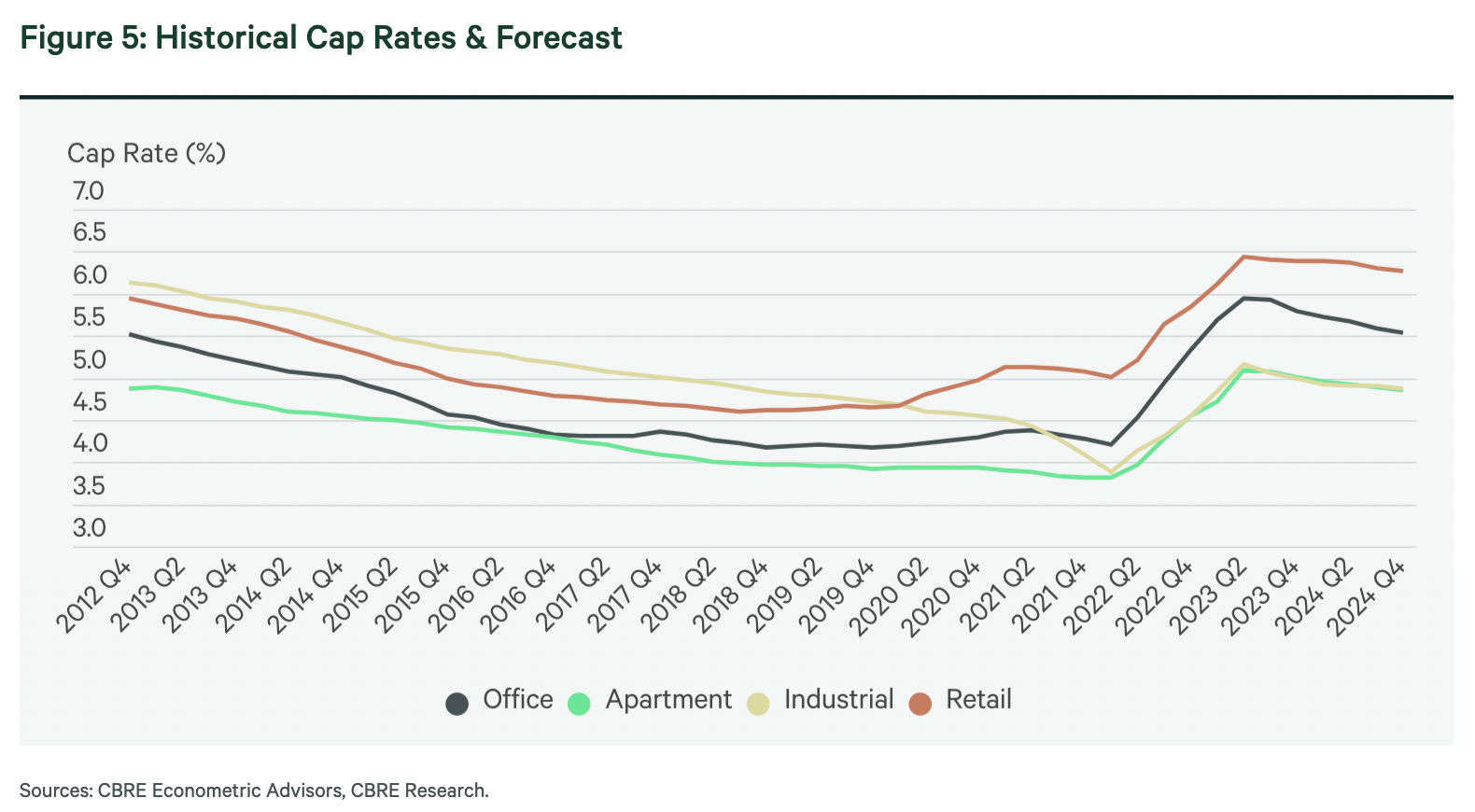

Rents tend to keep pace with inflation over the long term, making commercial real estate relatively attractive in times of high inflation. However, real estate asset values fall when interest rates rise, as tighter financial conditions inhibit economic activity and real estate demand. Since bottoming in early 2022, cap rates are up by approximately 100 basis points (bps) across all property types, translating to a 10% to 15% decline in values through the first three quarters of 2022. CBRE forecasts cap rates may expand by another 25 to 50 bps next year, which translates to roughly another 5% to 7% decrease in values.

Due to their relatively strong fundamentals and positive long-term demand outlook, multifamily and industrial properties will remain the most favored by investors. Grocery-anchored retail centers will also remain attractive following a decade of restrained development that bolstered fundamentals and has left the sector well positioned to weather a downturn. Investors will remain more discerning between high-end Class A office assets, which continue to have relatively strong fundamentals, and Class B and C office assets, which are showing signs of distress.

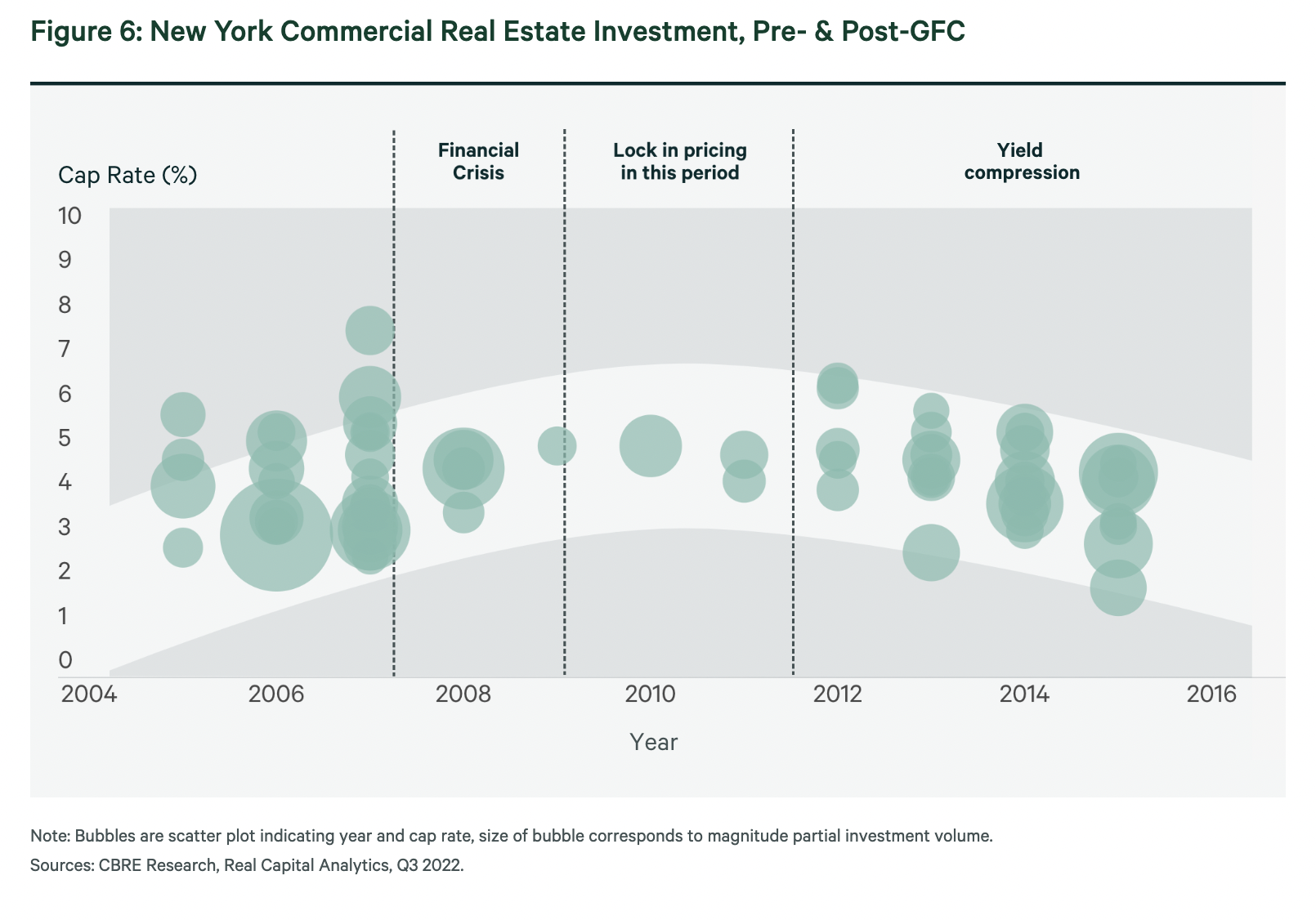

While higher capital costs will deter some buyers, there will be opportunities for large equity players who can deploy capital quickly. However, these investors will likely have a short window: Following the Great Recession, the trough in pricing only lasted around six to nine months before cap rates began to compress. Given expectations for a relatively moderate recession, the window of opportunity may be even shorter this time.

Investment activity will bottom out in early 2023

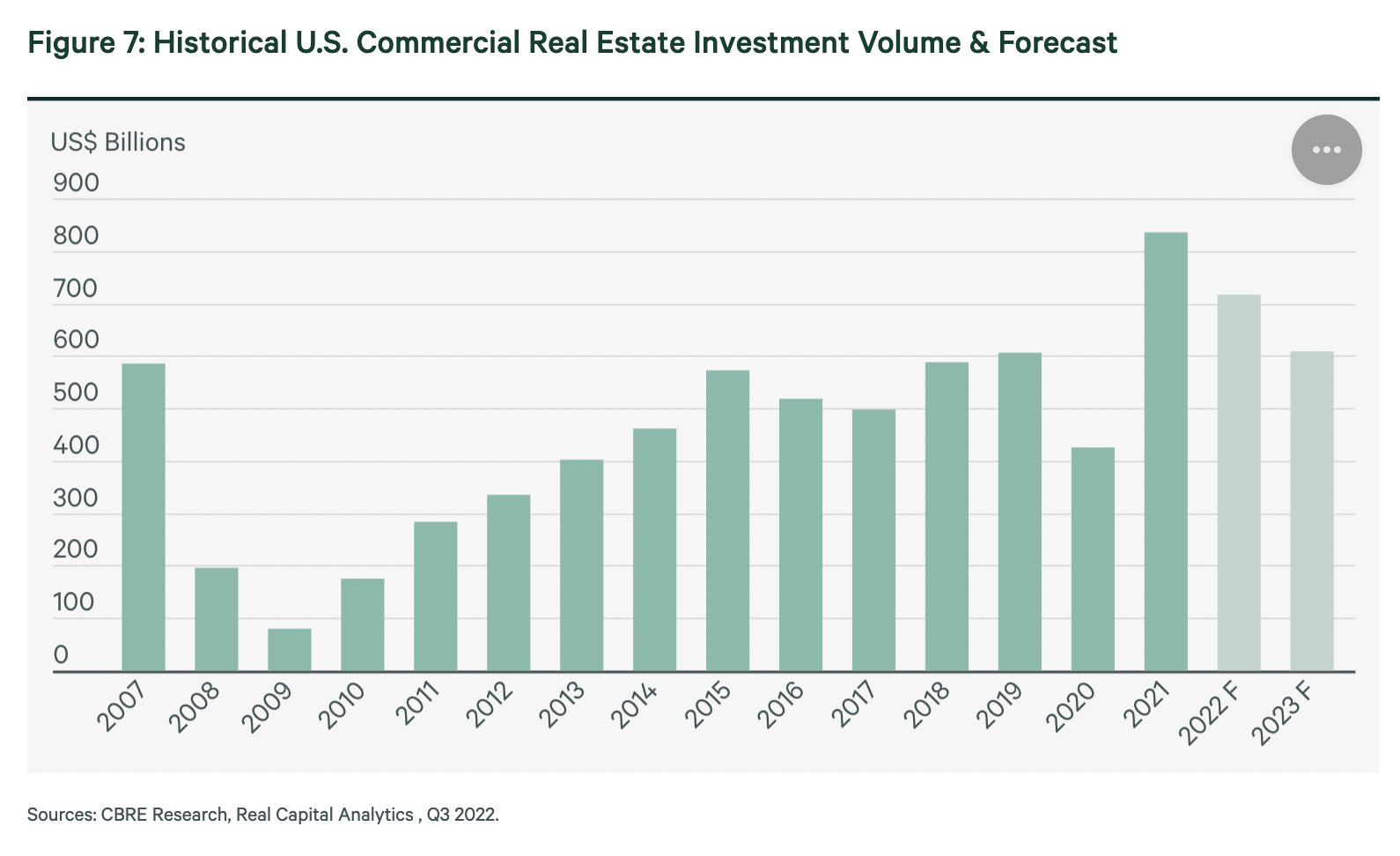

CBRE forecasts a 15% year-over-year drop in U.S. commercial real estate investment volume in 2023, although it will exceed the pre-pandemic record annual total in 2019. Investment activity likely will bottom out in the first quarter and then gradually improve. This timing assumes a moderate recession, lower inflation, a drop in long-term U.S. Treasury yields and the end of rapid-fire interest rate hikes. All of this will result in a less-uncertain environment, bolstering investor sentiment and facilitating sound underwriting.

Trends to Watch

Discerning Buyers

Multifamily and industrial will continue to enjoy structural tailwinds, which will underpin investor preference for those property types. Grocery-anchored retail will also fare well as investors gravitate toward relative strength in the market. Office investors will continue to prefer high-end Class A buildings.

Waning Uncertainty

By Q2 2023, a clearer picture should emerge about the terminal (max) federal funds rate and the overall economic outlook. Long-term yields and spreads should help reduce capital cost and allow for more sound underwriting. As a result, we expect quarter-over-quarter improvements in capital markets activity starting in Q2.